The Commodity Futures Trading Commission (the CFTC or Commission) issued a notice of proposed rulemaking on June 10, 2026, seeking public comment on proposed amendments to CFTC Regulation 40.11.1 The proposed amendments further specify the types of event contracts that may be subject to a public interest determination under Section 5c(c)(5)(C) of the Commodity Exchange Act (CEA), i.e., the "Special Rule" that authorizes the CFTC to prohibit the trading or clearing of certain event contracts on or through CFTC-registered entities.2

The Commission interprets the Special Rule to require a three-step inquiry. First, the Commission must assess whether the agreement, contract, transactions, or swaps in an excluded commodity is "based upon an occurrence, extent of an occurrence, or contingency."3 Second, the Commission must determine whether the event contract "involve[s]" one of the activities enumerated in the Special Rule (the Enumerated Activities). Those activities are "activity that is unlawful under any Federal or State law," "terrorism," "assassination," "war," "gaming," or "other similar activity determined by the Commission . . . to be contrary to the public interest."4 Finally, the Commission may prohibit a listing only after undertaking a public interest analysis and affirmatively determining that the event contract is affirmatively against the public interest.5

The proposed amendments clarify the Commission’s considerations at each step. Among other things, the proposed amendments define "involve" and "gaming" and set out the factors the Commission will weigh in deciding whether an event contract is contrary to the public interest.6 The proposed amendments also establish a 90-day review process, along with procedural safeguards for that review.7 The notice of proposed rulemaking contemplates that comments must be received by July 27, 2026.8

This advisory analyzes key aspects of the proposed amendments, evaluates their potential impact on current enforcement actions and litigation, and provides observations for market participants, designated contract markets (DCMs), and other stakeholders in the prediction markets space.

1. Stated Objectives of the Proposed Rulemaking and the Commission's Statutory Basis

The current proposed rulemaking follows two Commission releases on event contracts, both issued on March 12, 2026:

- First, Staff Advisory Letter No. 26-08 (the Advisory) provided the views of the Commission's Division of Market Oversight (DMO) on the listing and trading of event contracts.9 The Advisory reminded DCMs that CEA Section 5c(c)(5)(C) grants the Commission the ability to "determine that an event contract is contrary to the public interest if the contract involves, among other things, assassination, war, or terrorism," and that no contract determined by the Commission to be contrary to public interest may be listed or made available for clearing or trading on or through a registered entity.10 The Advisory also reminded DCMs of their various regulatory obligations under the CEA, including the obligation to conduct real-time monitoring of trading activity on its trading platform and to list only contracts that are not readily susceptible to manipulation.11

- Second, the Commission published an Advanced Notice of Proposed Rulemaking (ANPRM) that sought comments on a variety of topics related to event contracts, including standards for determining when contracts are "contrary to the public interest."12 The comment period for the ANPRM closed on April 30, 2026.13

The proposed amendments, consistent with the Advisory and ANPRM, reflect the Commission's goal of "reduc[ing] ambiguity" around event contract regulation, including with respect to the scope of the Special Rule.14 The Commission anticipates that these ostensibly more transparent rules will "generate tangible administrative efficiencies for prediction markets and market participants," including "shorter review cycles, fewer scope-related disputes, and reduced risk of post-listing reversals,"15 while also supporting responsible innovation in prediction markets.16 The Commission issued its proposal pursuant to its "exclusive jurisdiction" grant under the CEA,17 and in accordance with "CEA Sections 3, 5, 5c(c), 5h, and 8a(5),"18 which allow the Commission to regulate derivatives, exchanges, event contracts, and clearing facilities.

2. New Definitions

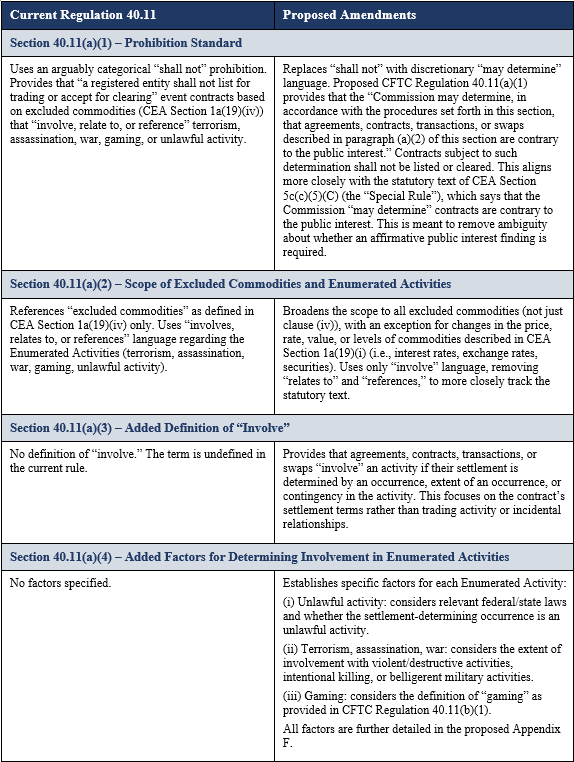

The proposed amendments to CFTC Regulation 40.11 add two concepts that do most of the work of narrowing the Special Rule. The first defines when an event contract "involves" an Enumerated Activity. Under the proposed standard, the Commission would look to whether settlement depends on an occurrence, the extent of an occurrence, or a contingency in the activity itself, rather than on the act of trading the contract or on an incidental relationship to the activity.19

The proposed standard makes the contract's settlement terms central to the analysis. For example, a contract on whether a football player scores a set number of touchdowns would "involve" gaming because settlement turns on something that happens in the game.20 A contract on game attendance would not involve gaming, because settlement turns on ticket-purchasing decisions made outside the game.21 The same logic appears in the Commission's examples involving terrorism, assassination, and war. A contract involves assassination if it settles based on whether a foreign leader dies as a result of a political attack.22 The Commission also expressed its view that a contract with a facially neutral settlement mechanism involves Enumerated Activity if a settlement pathway can be satisfied through one of those Enumerated Activities. For example, a contract that settles based on whether a foreign leader is out of office by a certain date would, in the Commission’s view, involve assassination because that is "among the pathways by which the settlement condition can be satisfied."23 The contract would not involve assassination if it was redrafted to specify that the settlement pathways are limited to electoral defeat, resignation, constitutional removal, negotiated departure, natural death, government demolition, or diplomatic resolution.24

The second key definition is "gaming." The Commission proposes to define gaming as an activity that participants typically engage in for recreation or to entertain others, that is governed by rules, and that includes measurable outcomes that depend on luck, skill, or athletic ability during the activity.25 The Commission distinguishes gaming from gambling by treating gaming as the game underlying the event contract, rather than the act of staking value on a contingent outcome. That distinction is important because a wagering-based definition of gaming would risk treating every event contract as gaming, which the Commission noted would leave the Special Rule without a meaningful boundary.26

The proposed gaming definition also distinguishes games from contests. The Commission states that elections, awards, and similar contests do not become gaming simply because people may wager on them. It requests public comment on more difficult edge cases, including game shows, reality show competitions, pageants, music competitions, talent competitions, and competitions whose outcomes depend on judges or scoring formulas. As a result, questions remain for entertainment products that mix rules, judging, skill, audience appeal, and commercial promotion.

3. Public Interest Factors and Contracts That Are Per Se Contrary to the Public Interest

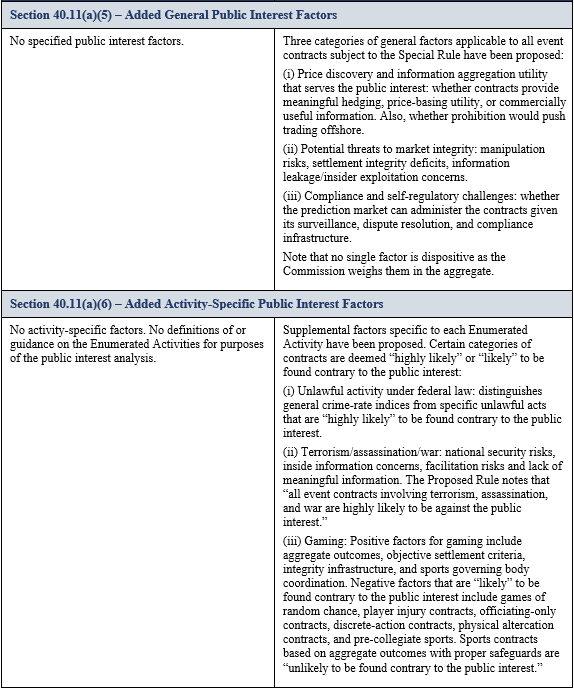

The proposed amendments establish a multi-factor public interest analysis that the Commission would apply when determining whether event contracts involving Enumerated Activities are contrary to the public interest. No single factor is dispositive. The Commission would weigh them in the aggregate, recognizing the diversity and complexity of event contracts that could fall within the Enumerated Activities.27 The Commission organizes these factors into two tiers: (1) general factors applicable to all event contracts subject to the Special Rule, and (2) factors specific to particular Enumerated Activities.28

General Public Interest Factors.

Proposed CFTC Regulation 40.11(a)(5) sets out three categories of factors applicable to all event contracts subject to the Special Rule.29

- First, the Commission would assess whether the event contracts serve the public interest by providing meaningful hedging or price-basing utility, yielding economically, financially, or commercially useful information, or promoting responsible innovation and fair competition.30 The Commission stressed that prediction markets function as "information aggregation vehicles" and that an event contract need not demonstrate a direct hedging purpose. What matters instead is whether pricing information from the contracts can guide hedging or other economic decisions.31 The Commission would also consider whether prohibiting an event contract would push trading activity into less transparent, less regulated foreign markets, a factor weighing against a contrary-to-public-interest finding.32

- Second, the Commission would evaluate whether the event contracts present particular risks of manipulation or market disruption, exhibit settlement integrity deficits, or create particular risks of information leakage or exploitation of material nonpublic information by insiders.33 This factor is distinct from the requirement under the DCM Core Principles that DCMs list only contracts not readily susceptible to manipulation. Instead, it asks whether, in the specific context of event contracts involving Enumerated Activities, the contracts' characteristics raise heightened public interest concerns regarding manipulation, settlement ambiguity, or exploitation of insider information.34

- Third, the Commission would consider whether trading or clearing the event contracts would challenge the prediction market’s self-regulatory tools or compliance infrastructure.35 This factor examines whether a DCM, given its existing compliance, surveillance, and dispute-resolution infrastructure, can discharge its statutory self-regulatory obligations with respect to the event contracts. Guardrails reasonably designed to address specific risks, such as prohibiting certain categories of traders with access to inside information, maintaining robust surveillance and customer identification policies, and establishing suitable dispute resolution procedures, would weigh against a finding that the contract is contrary to the public interest.36

Activity-Specific Factors and Contracts Likely To Be Found Contrary to the Public Interest.

In addition to the general factors, proposed CFTC Regulation 40.11(a)(6) sets forth factors specific to each Enumerated Activity.37 The Commission identifies certain categories of contracts that are "highly likely" or "likely" to be found contrary to the public interest.

- Terrorism, assassination, and war. The Commission states that "all event contracts involving terrorism, assassination, and war are highly likely to be against the public interest."38 Such contracts could encourage violent activity by creating financial incentives, present extreme information leakage risks and settlement uncertainty (e.g., the "fog of war"), and allow market participants to profit from potential assassination or acts of terrorism.39

- Games of random chance. The Commission states that event contracts involving games that depend entirely on random chance are "highly likely" to be found contrary to the public interest.40 Because participants have no insight to contribute when outcomes are dictated solely by luck, such contracts provide no meaningful information and do not advance any CEA purpose. Games that depend significantly on luck but are also meaningfully affected by skill, such as poker tournaments, would be treated differently.41

- Activity unlawful under federal law. The Commission states that event contracts involving activity unlawful under federal law are "highly likely" to be found contrary to the public interest, except where the contracts reference generalized crime rates over time in a manner that does not incentivize specific criminal conduct.42 The Commission reasons that permitting trading in contracts involving activity Congress has determined to be illegal is likely contrary to the public interest.43

- Certain sports-related event contracts. The Commission identifies several categories of sports-related event contracts as "likely" to be found contrary to the public interest. Player injury contracts could create financial incentives to cause physical harm. Officiating-only contracts present significant manipulation and subjectivity concerns. Discrete-action or "first-action" contracts, tied to a single player's in-game decisions, let one individual determine how the contract settles. Physical altercation contracts could incentivize violent conduct, and pre-collegiate sports contracts raise concerns about the manipulation of minors and the absence of a developed integrity infrastructure.44

By contrast, the Commission views event contracts based on the aggregate outcomes of professional or collegiate sports events, such as final scores, point differentials, win-loss results, tournament advancement, and season-long performance metrics, as "unlikely to be found to be contrary to the public interest." That view assumes the contract settles on objective and verifiable criteria and that the prediction market maintains appropriate surveillance, enforces trading prohibitions, and coordinates with the relevant sports governing bodies.45 This preliminary view does not create a safe harbor but reflects the Commission’s assessment of how the factor analysis generally resolves for such contracts.46

The Commission's preliminary view on aggregate sports outcomes is meant to distinguish permissible event contracts from potentially problematic ones. DCMs that maintain appropriate surveillance, enforce trading prohibitions, and coordinate with relevant sports governing bodies will find a clearer path to listing. The Commission has already laid the groundwork for this model, including its recent Memoranda of Understanding (MOU) with Major League Baseball47 and the National Hockey League, the first agreements of their kind between the CFTC and a professional sports league, that establish frameworks for information sharing and integrity coordination. These MOUs provide the institutional infrastructure for the cross-industry collaboration that the proposed rule treats as a mitigating factor in the public interest analysis. For DCMs listing sports-related event contracts, engaging with league integrity units and establishing data-sharing arrangements will likely become a practical prerequisite, not merely a recommendation.

4. Proposed Determination Process

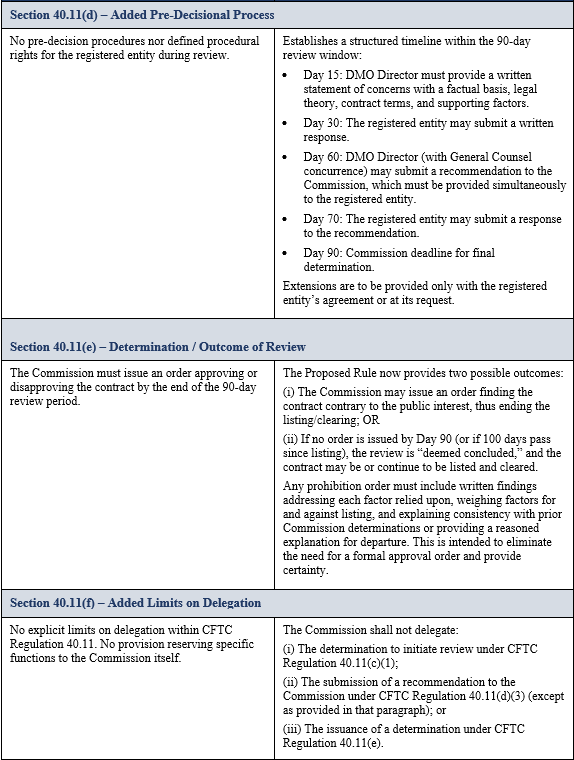

The proposed amendments would also create a defined process for deciding whether to prohibit a contract from listing or clearing. This differs from the current CFTC Regulation 40.11, which some read to impose a categorical prohibition on any contract that involves an Enumerated Activity before it is listed for trading on a DCM. Under the proposal, the Commission may begin review only through a written determination that a contract submitted under CFTC Regulation 40.2 or 40.3 both involves an Enumerated Activity and may be contrary to the public interest. The review must begin within 10 days after the contract is listed.48

The Commission's written determination would start the clock on the formal process by first identifying the contract, the relevant Enumerated Activity, the contract terms at issue, and the factors that warrant review. The proposal would then establish deadlines based on the date of that written determination. Within 15 days, the Director of the DMO must provide the registered entity with a written statement of concerns that identifies the factual basis, legal theory, contract terms, and factors supporting the review.49 Within 30 days after the review begins, the registered entity may submit a written response, including supporting data, expert materials, economic analysis, proposed contract changes, or mitigating safeguards.50 Within 60 days after the review begins, the DMO Director, with the concurrence of the General Counsel of the Commission, may submit a recommendation to the Commission, and the registered entity may respond to that recommendation within 70 days.51

The Commission must make any final public interest determination within 90 days after the review begins, unless the submitting registered entity agrees to an extension.52 If the Commission issues an order finding the contract contrary to the public interest, the contract may not be listed, traded, or accepted for clearing. If the Commission does not issue an order by the end of the review period, or if 100 days have passed since the date of the listing of the contract, the review ends and the contract may be listed or continue trading and clearing.53

The proposal would also allow the Commission to review similar contracts together.54 The Commission could consolidate contracts that involve the same underlying event or a substantially similar set of underlying events, and could issue one order covering the group. That approach would give registered prediction markets a more useful precedent when they design contracts; however, the Commission would need to describe the covered group clearly enough for market participants to understand which later submissions raise the same concerns.

A practical risk remains because trading may continue while the Commission reviews a contract. Under CFTC Regulation 40.2, a registered entity may list a self-certified contract for trading on the business day after it submits the certification to the Commission. The proposal would allow the Commission to request that the registered entity suspend listing or trading during review, but the registered entity would not be required to agree.55 If the Commission later finds the contract to be contrary to the public interest, market participants would likely be required to liquidate their positions and lose any hedges or unrealized gains. To reduce that risk, the Commission encourages registered entities to consult with Commission staff before self-certifying contracts that may involve an Enumerated Activity and raise public interest concerns.

5. Potential Impacts

A. New Product Listing Considerations

The proposed rulemaking would make event contract self-certification submissions more important for new products, especially for contracts that may involve an Enumerated Activity. The Commission noted that many event contracts currently rely on template submissions that describe broad product families.56 For contracts that potentially involve an Enumerated Activity, the Commission signaled that a general template may not provide staff enough information to conduct a CFTC Regulation 40.11 review or satisfy the requirement to explain why the contract complies with the CEA.

Registered entities should expect to map each product's settlement trigger to the Commission's proposed "involves" test and then address the public interest factors in the certification record. That record should explain why the contract has price discovery, information aggregation, hedging, or other commercial utility, why the settlement criteria are objective and publicly verifiable, and how the product avoids concentrated control, settlement ambiguity, and insider information risks. The strongest submissions will likely look less like generic template filings and more like product-specific regulatory analyses.

Sports-related event contracts will require particularly careful drafting under the public interest analysis. The Commission gave the clearest path to contracts based on aggregate professional or collegiate sports outcomes, such as final scores, point differentials, win-loss results, tournament advancement, individual or team statistical performance, and season-long metrics.57 By contrast, product designs that settle solely on player injuries, officiating decisions, discrete actions, physical altercations, or pre-collegiate outcomes would weigh strongly in favor of a Commission finding that the contract is contrary to the public interest.58

The proposed rulemaking also rewards operational readiness. A registered entity that can show robust surveillance, customer identification, prohibited-trader controls, dispute resolution, reliable settlement feeds, and information-sharing arrangements will be better positioned to argue that any residual public interest concerns have been mitigated.59 Product teams should therefore treat legal analysis, market surveillance, data sourcing, and external coordination as part of the listing process rather than as post-listing compliance work.

B. Encouraging Institutional Participation

The proposed rulemaking may significantly affect institutional participation in prediction markets. By establishing a transparent, multi-factor framework for evaluating event contracts, the Commission aims to reduce the regulatory uncertainty that has deterred institutional investors, banks, and traditional financial intermediaries from entering the space.60

The prediction markets industry has grown explosively, with total trading volume across CFTC-registered prediction markets exceeding $25 billion in 2025 and event contract listings increasing from approximately 1,600 per day in April 2025 to 162,000 per day in April 2026.61 The Commission has reviewed 28 DCM and SEF applications in the past year, approving 7 DCMs, with 18 DCM applications and 3 SEF applications still under review.62

The proposed amendments are designed to support this institutional growth in several ways. First, the new framework provides “clearer boundaries for lawful versus prohibited products,” which the Commission expects will result in “shorter review cycles, fewer scope-related disputes, and reduced risk of post-listing reversals.”63 For futures commission merchants (FCMs) seeking to intermediate prediction market transactions, this regulatory certainty is critical because firms cannot allocate capital, build compliance infrastructure, or onboard customers around product lines facing uncertain regulatory fates.64

Second, the proposed rulemaking builds on the self-regulatory role of prediction markets, setting benchmarks that sophisticated institutional entrants can readily meet.65 Specifically, the Commission would evaluate whether a prediction market maintains surveillance systems capable of detecting abnormal trading patterns and insider information risks.66 The Commission would also assess whether its customer identification and account monitoring systems are sufficient to link trading activity to individuals or entities and to distinguish insiders.67 Additionally, the Commission would consider whether its dispute-resolution processes are adequate to resolve settlement disputes.68 The Commission would also examine whether the prediction market has access to reliable settlement feeds with mechanisms to validate data integrity.69 The Commission acknowledges that smaller or newer prediction markets may face disproportionate burdens in scaling these capabilities, potentially advantaging incumbents with existing compliance infrastructure.70 For large financial institutions and established FCMs considering entry into prediction markets, the compliance expectations are substantially similar to obligations they already fulfill in traditional derivatives markets.

Third, the Commission recognizes that event contracts serve hedging and price-basing functions for businesses seeking to hedge exposure to legislative, regulatory, and policy actions, as well as for commercial participants in sports-adjacent industries such as broadcasters, sponsors, advertisers, and analytics firms. This acknowledgment lends legitimacy to prediction markets, which may encourage institutional adoption.71 The Commission expressly notes that "market participants have demonstrated demand for event contracts addressing categories of risk for which traditional financial instruments either do not exist or provide only imperfect hedges with substantial basis risk."72 This framing positions prediction markets as instruments that serve genuine commercial functions within the broader derivatives ecosystem, rather than as speculative novelties.

The proposed rule acknowledges competitive dynamics that directly affect institutional participation. The Commission notes that competition among prediction markets "can create incentives to differentiate by offering broader event contract selections, including designs that test the boundary of acceptability."73 Uniform enforcement would reduce concerns about a regulatory race to the bottom. Yet the Commission also recognizes that "scale economies in integrity tooling could advantage incumbents" and that "unequal access to league-verified data or integrity arrangements could create de facto asymmetries."74

C. Enforcement and Litigation

The proposed amendments carry several implications for litigation and enforcement related to event contract trading.

First, although the Commission reaffirmed its commitment to ensuring "its regulations protect market participants and the public,"75 the Commission ties that goal to its aim of providing "clearer boundaries for lawful versus prohibited products."76 By shifting its focus from post-hoc enforcement to early review of event contracts, the Commission hopes to limit the "probability that problematic event contracts may be listed," and reduce "litigation risk and regulatory uncertainty" for DCMs and market participants.77

Second, the proposed public interest factors, which focus on potential threats to market integrity, including "risks of information leakage or exploitation of material non-public information by insiders or identifiable persons capable of influencing outcomes"78 reflect "heightened DCM and Commission scrutiny of insider trading, manipulation, and surveillance sufficiency in prediction markets."79 These proposed changes follow two recent CFTC insider trading lawsuits. In the first, the CFTC alleged that Gannon Ken Van Dyke, an active-duty U.S. Army service member, used classified nonpublic information about U.S. operations to capture former Venezuelan President Nicolás Maduro and his wife, Cilia Flores, to trade on an offshore prediction market.80 In the second, the CFTC alleged that Michele Spagnuolo traded on sensitive nonpublic information he acquired through his employment with Google.81 The proposed changes make clear that regulation of insider trading remains a priority for the Commission, consistent with Chairman Selig's warning that "anyone who engages in fraud, manipulation, or insider trading in any of our markets will face the full force of the law."82

Third, the proposed amendments expressly reaffirm the Commission's "exclusive jurisdiction" over event contracts.83 The Commission’s proposal to define terms like "gaming" makes clear the CFTC's intent to wholly regulate event contract trading. These proposed amendments affect pending prediction markets cases brought by state attorneys general and gambling recovery limited liability companies seeking to enforce state gaming or gambling laws against DCMs and FCMs.

D. Federal Preemption and Exclusive Jurisdiction

The proposed rule lands in the middle of a jurisdictional contest over who regulates prediction markets, and it comes down firmly on the side of federal authority. The Commission invokes its “exclusive jurisdiction” under the CEA and states that the CEA preempts state laws that attempt to regulate the operation of, or transactions on, CFTC-registered exchanges.84 By treating activity that is unlawful under state law as one factor in its public interest analysis rather than as a basis for deferring to state regulators, the rule leaves little room for state gaming and wagering authorities to assert control over event contracts traded on a DCM.85 That position aligns with the Third Circuit, which has held that the CEA grants the CFTC exclusive authority over event contracts and brings their trading on registered exchanges within a unified federal scheme.86

The same framework answers the objections of tribal and gaming-industry opponents. Because the proposed definition of gaming separates playing a game from wagering on its outcome, event contracts that settle on sports results do not "involve" gaming merely because they resemble sports bets, which undercuts the central argument of state-licensed sportsbooks that prediction markets offer functionally identical products outside state licensing and tax regimes.87 The Commission acknowledges the Indian Gaming Regulatory Act and the importance of gaming revenue to tribal governments and invites comment, but it maintains that event contracts traded as swaps or futures fall within its exclusive jurisdiction.88 The practical takeaway for market participants is that the Commission is asserting comprehensive federal authority over event contracts and is positioning that authority to withstand the continuing challenges from opponents of preemption.

E. Issues Not Addressed (Future Rulemakings)

Several issues remain open for future rulemaking or further Commission action. The proposal did not identify any new activity as "similar" to the Enumerated Activities, but it expressly preserved the Commission's authority to do so by rule or regulation. That means the current proposal gives market participants a framework for comparing future activities to unlawful activity, terrorism, assassination, war, and gaming, but it does not close the door on additional categories if the Commission later concludes that a new class of event contracts presents comparable public interest concerns.

The proposal also asks whether the Commission should add broader procedures that would apply before a particular contract is self-certified. One possibility would allow the Commission to make a category-level public interest determination for a defined class of event contracts involving an Enumerated Activity, even before a registered prediction market submits a specific contract.89 Another possibility would be to use the Commission's exemptive authority under CEA Section 4(c) to identify defined classes of event contracts that may trade without individualized review under CFTC Regulation 40.11.90 The final rule may adopt neither option, but comments on these alternatives could shape how much review occurs at the category level rather than on a contract-by-contract basis.

The proposal also asked for comment on entertainment and technology questions that it does not resolve in the proposed rule text. For entertainment products, the Commission asked whether game shows, reality competitions, pageants, and similar events should count as gaming.91 It also offered an alternative definition under which gaming would mean an activity created by its rules, where the participants who determine the outcome act within the activity and pursue objectives internal to that activity. For technology-related issues, the Commission asked whether registrants should monitor matters such as data provenance, automated quoting, AI-generated content, synthetic polling, deepfakes, anomaly detection, and offshore migration.92

6. Comment Period and Proposed Implementation Issues

Comments on the proposed rulemaking are due July 27, 2026. The Commission requested comment on all aspects of the proposal, including the "involves" standard, the "gaming" definition, the public interest factors, the process for Commission review, potential alternatives to individualized review, and the costs and benefits of the proposed approach.

The proposed implementation timeline gives registrants some, but not much, time to adjust. The Commission proposed that the amendments would take effect 60 days after publication of a final rule in the Federal Register, at which point staff would begin reviewing certified event contracts under the new framework.93 Registered entities should use the comment period and the period before any final rule to inventory existing and planned products, identify which products may involve an Enumerated Activity, and update certification processes so future submissions address the proposed factors.

The proposed timeline also gives registered entities little room to build the record after the Commission begins its review. If the Commission initiates a review, the DMO Director would provide a statement of concerns within 15 days after the review's start, and the registered entity may submit its response within 30 days after the review's start. A registered entity that waits until review begins to assemble legal analysis, settlement data, surveillance materials, expert support, proposed contract changes, or mitigating safeguards may lose the chance to shape the record effectively. Registered entities should build a standing file for each higher-risk product that addresses settlement data, information controls, surveillance, dispute resolution, trader eligibility, and any third-party coordination before certification.

7. Section-by-Section Analysis (Appendix)

Screenshot 2026-06-26 114804.png)

1 Prediction Markets; Public Interest Determinations, 91 Fed. Reg. 35,806 (June 12, 2026) ("Proposed Rule").

2 See Katten Associate Alexander Kim's AI-generated visualization of the types of event contracts that may be subject to a public interest determination under Section 5c(c)(5)(C) of the CEA here.

3 Id. at 35,810-11.

4 7 U.S.C. § 7a-2 (c)(5)(C)(i)(I)-(VI).

5 Proposed Rule at 35,811.

6 Id. at 35,840.

7 Id.

8 Id. at 35,806.

9 CFTC Letter No. 26-08 (Mar. 12, 2026), available here.

10 Id.

11 Id.

12 CFTC Release No. 9194-26, CFTC Seeks Public Comment on Advance Notice of Proposed Rulemaking Relating to Prediction Markets (Mar. 12, 2026), available here.

13 See Katten Associate Alexander Kim’s AI-generated analysis of public comments submitted in response to the ANPRM here.

14 Proposed Rule at 35,846.

15 Id. at 35,8-45.

16 Id. at 35,848.

17 Id. at 35,859.

18 Id. at 35,818 (citing 7 U.S.C. §§ 5, 7, 7a-2(c), 7b-3 and 12a (5)).

19 Id. at 35,821.

20 Id. at 35,864.

21 Id.

22 Id. at 35,824.

23 Id.

24 Id. at 35,824.

25 Id. at 35,826.

26 Id. at 35,863.

27 See id. at 35,828-29.

28 Id.

29 Id. at 35,829.

30 Id.

31 Id. at 35,829-30.

32 Id. at 35,831.

33 Id. at 35,832.

34 Id.

35 Id. at 35,833.

36 Id.

37 Id. at 35,834.

38 Id. at 35,834-35.

39 Id.

40 Id. at 35,835.

41 Id. at 35,835.

42 Id. at 35,833-34.

43 Id.

44 Id. at 35,836-37

45 Id. at 35,835-36.

46 Id. at 35,836.

47 See Katten's coverage of the MLB MOU here.

48 Id. at 35,819.

49 Id. at 35,861.

50 Id.

51 Id.

52 Id.

53 Id.

54 Id.

55 Id. at 35,818.

56 Id. at 35,847.

57 Id. at 35,853.

58 Id. at 35,870.

59 Id. at 35,851-52.

60 See id. at 35,846.

61 Id. at 35,844.

62 Id.

63 Id. at 35,8444-45.

64 See id. at 35,846.

65 Id. at 35,851.

66 Id.

67 Id.

68 Id.

69 Id.

70 Id. at 35,852.

71 Id. at 35,831, 35,836.

72 Id.

73 Id. at 35,856.

74 Id.

75 Id. at 35,855.

76 Id. at 35,846.

77 Id. at 35,846, 35,853. The proposed amendments follow Kalshi’s summary judgment win against the Commission in the District of Columbia in 2024. Kalshi had challenged an order issued by the Commission, prohibiting it from listing certain political event contracts on the grounds that its event contracts were contrary to the public interest under the Special Rule. The District Court granted Kalshi’s summary judgment motion and vacated the Commission’s decision, ruling that Kalshi’s contracts “d[id] not involve activity that is unlawful under any Federal or State law, nor do they involve gaming.” The CFTC appealed the District Court decision but subsequently voluntarily dismissed the case. The CFTC’s voluntary dismissal of its appeal in the Kalshi case and the current proposed amendments both signal a willingness on the part of the Commission to work with DCMs prior to litigation to ensure that event contracts are properly listed and traded.

78 Id. at 35,849.

79 Id. at 35,846.

80 See Katten’s coverage of the Van Dyke case here.

81 See Katten’s coverage of the Spagnuolo case here.

82 CFTC Release No. 9217-26, CFTC Charges U.S. Service Member with Insider Trading in Nicolás Maduro-Related Event Contracts (Apr. 23, 2026), available here.

83 Proposed Rule at 35,808.

84 See Proposed Rule at 35,808.

85 See Proposed Rule at 35,833-34.

86 See Katten’s coverage of the Third Circuit ruling here.

87 See Proposed Rule at 35,826-27.

88 Proposed Rule at 35,858-59.

89 Id. at 35,839.

90 Id. at 35,839.

91 Id. at 35,827.

92 Id. at 35,858.

93 Id. at 35,843.